- Introduction

- Industrial Emissions

- Strategies to avoid process-based emissions https://t.co/7eOBQc25bA

- Policy instruments for enabling a climate-neutral industry https://t.co/CVekzrPmrT

- Conclusions

- Questions and answers https://t.co/rtg9jMLhlH

.@KWitecka from @AgoraEW on:

“Technology and policy options for a climate-neutral energy-intensive industry”

Options for the steel, cement and chemical industries

https://t.co/jwHgxaGVwl https://t.co/ywpj7FuJX8

Introduction

Industry has long been out of the discussion, why?

- “Hard to abate” -> high share of process emissions, new tech needed

- Allocation techniques: direct emissions (20 %) vs. higher if elec. + heat are allocated, making it the highest CO2 source

Rationale :

- Avoiding process emissions = key

- Long lifetime of industrial plants : future investment has to be in new technologies, otherwise no possibility of reaching the Paris agreement

Industrial Emissions

Worldwide

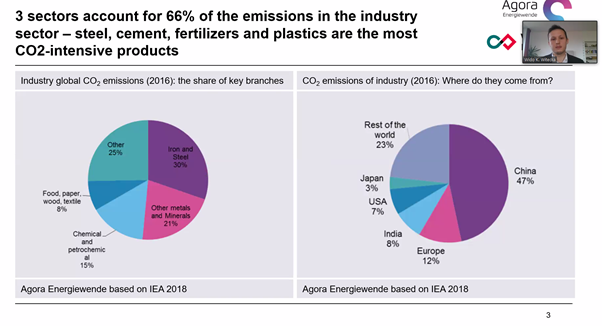

3 sectors account for 66 % of industrial emissions

Most CO2-intensive:

- Steel

- Cement

- Fertilizers

- Plastics

Where do they come from?

- China

- Europe

- India

- US

- Japan https://t.co/17IwWaEqxv

Germany

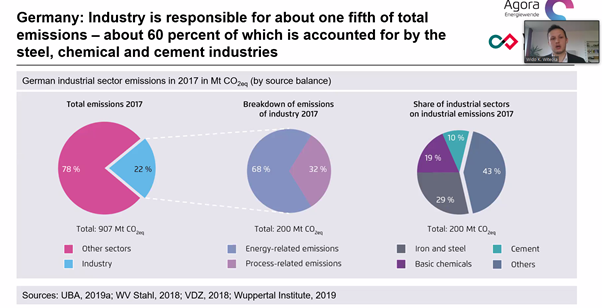

Industry emits 1/5th of national territorial emissions, of which 60 % are steel, chemicals and cement https://t.co/nGkiA5XGYD

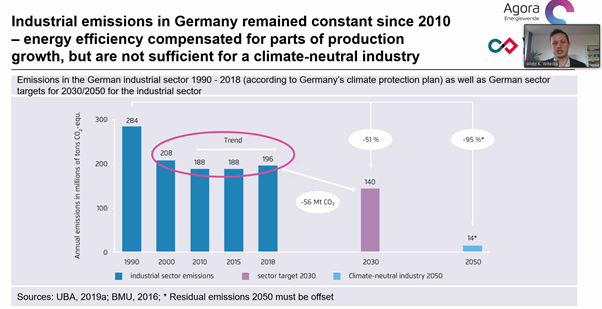

Despite energy efficiency measures, emissions stayed constant.

Energy efficiency measures are only able to compensate for continued demand.

This applies to a global scale.

If we believe in continued economic growth, energy efficiency measures are not sufficient. https://t.co/PbEDJY34l3

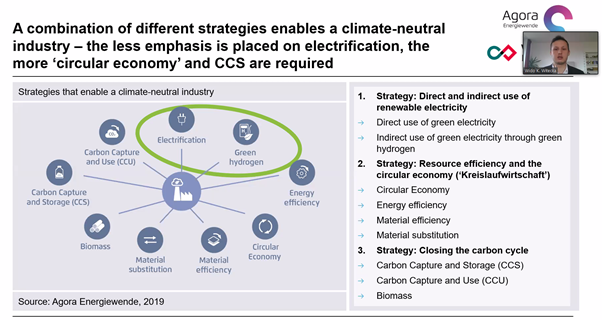

Strategies to avoid process-based emissions https://t.co/7eOBQc25bA

3 types of strategies:

- Direct/indirect electrification

- Resource use : circular economy, material substitution (wood, ..) –> major effect on energy use

- Carbon capture, utilization and use of sustainable biomass https://t.co/YC0tQjfWMS

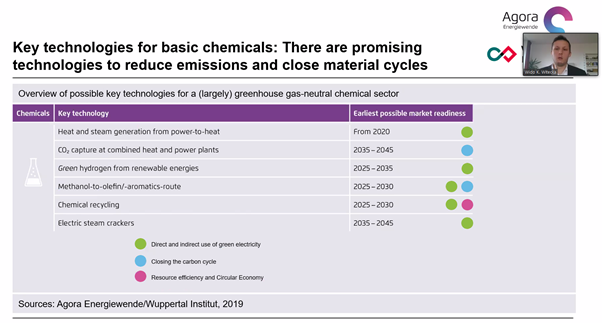

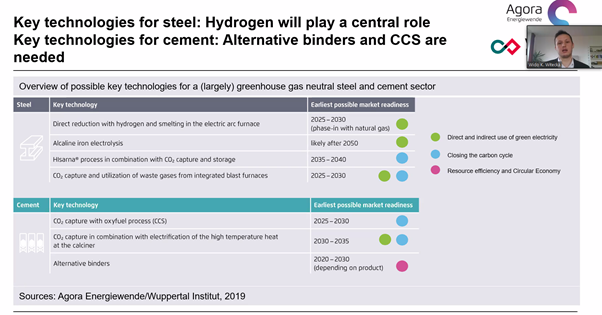

Key technologies

For..

- basic chemicals -> different technologies available

- steel -> hydrogen playing a central role

- cement -> carbon capture will still play an important role (if not replaced by other materials) https://t.co/rzEyAuEg9Z

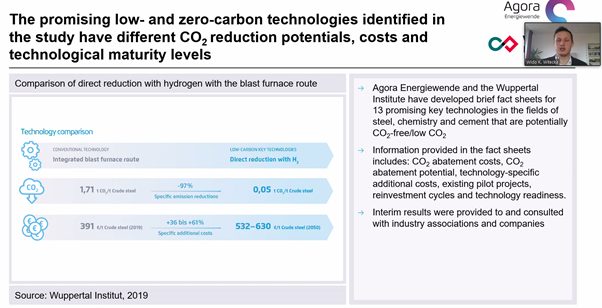

Costs : @AgoraEW study database with…

- Abatement potential

- Technology specific costs

- Technology readiness level https://t.co/rlQw2tZjQt

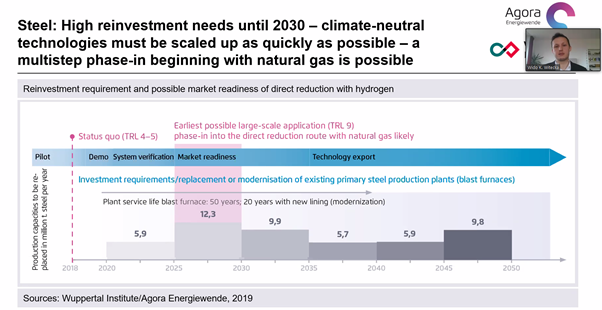

Industry re-investment needs

Example of steel: technology could be ready and deployed by 2025 from a technical point of view. Even if not enough green hydrogen available, temporarily natural gas could be used.

Important not to lift the re-investment cycle beyond 2025. https://t.co/JaTwdEQqil

European/German industry is working on different pilot plants, but large-scale deployment framework is missing https://t.co/E7nFVeDd8C

Policy instruments for enabling a climate-neutral industry https://t.co/CVekzrPmrT

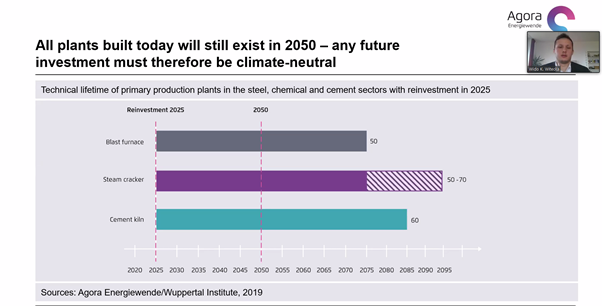

Key message: all plants that are built today, will still exist in 2050 (lifetimes of 20/30 tot 70 years are not unusual)

–> any future investment from now on must therefore be climate neutral https://t.co/SjUry8UqDq

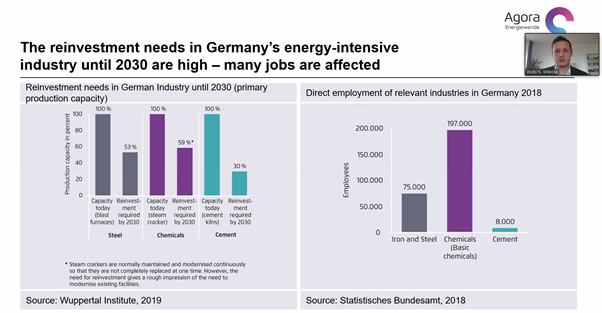

Re-investment need

Example : Germany.

53 % of steel infrastructure will need to be replaced by 2030 59 % for chemicals 30 % in cement-sector

Employment : lots of people are affected by investment decisions. Strategic decisions have big impacts. https://t.co/7Sp9nSwzBC

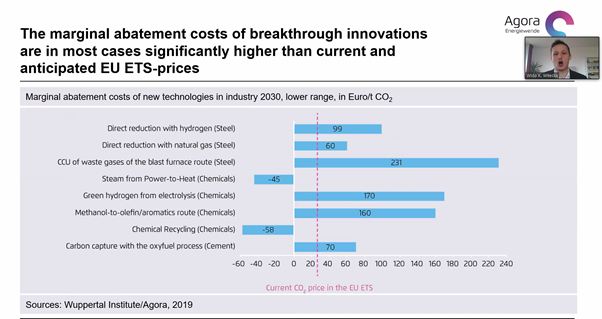

Marginal abatement costs and carbon price

…but marginal abatement cost of new technologies are significantly higher than conventional tech.

The CO2-price in the EU ETS is not enough to introduce these technologies to the market.

Therefore, other policy instruments needed. https://t.co/lLvvk34mlo

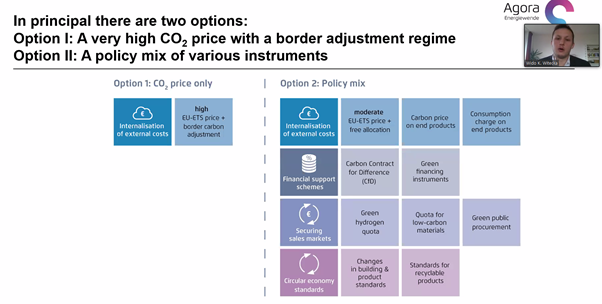

Other policy options

[I] High CO2-price with border adjustment, under discussion in Europe

[II] Policy mix:

- Carbon contract for difference: covering additional cost of green tech

- Green product markets: H2/low-carbon quota

- Circular economy: building/products standards https://t.co/BcsP0pcrdV

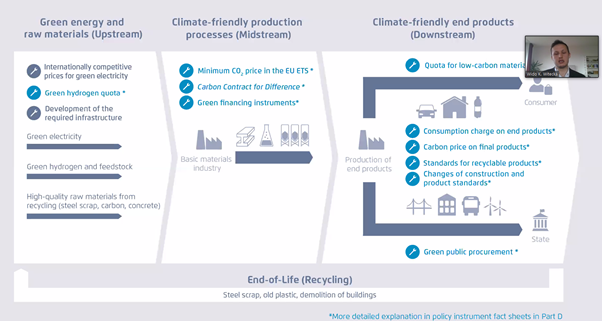

Industrial value chain perspective

Upstream -> competitive prices for electricity, infrastructure for CCS, green hydrogen quota Midstream -> minimum CO2 price, carbon contract for difference, green financing instruments Downstream -> low-carbon materials quota / standards https://t.co/zASuURECOj

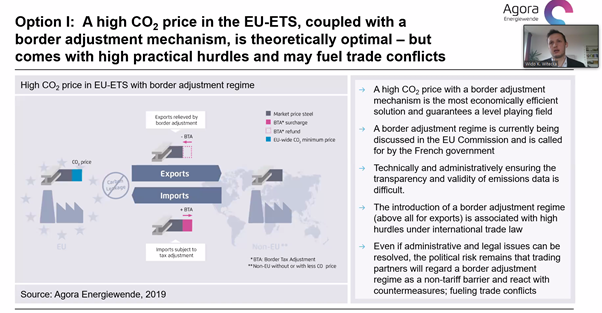

Option I : High CO2 price with border carbon adjustment

If basic materials are imported -> carbon adjustment

If export to other countries -> also border adjustment? Question if this is feasible (WTO)

Tracking of CO2 content needed: difficult administration, room for fraud https://t.co/PU7C5gFuYe

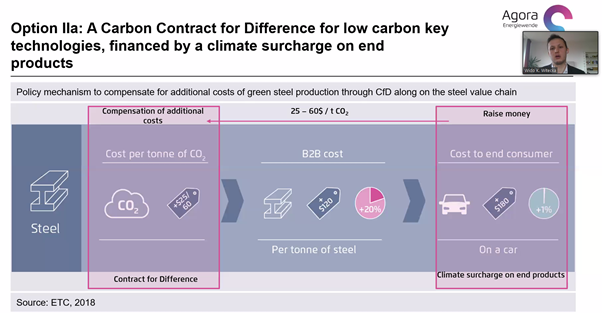

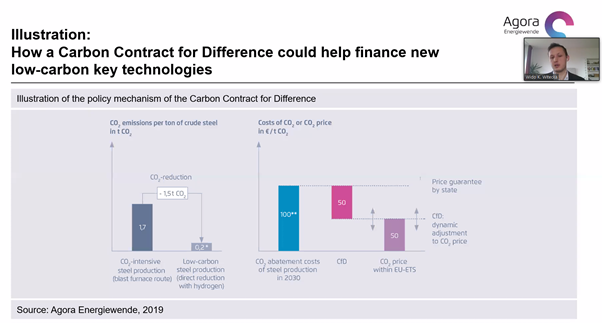

Option IIA: Carbon contract for difference

Money coming from carbon content surcharge on products https://t.co/IfTXCxkHez

Illustration for steel industry:

Break even of CO2 abatement around 100 EUR / tonne CO2

Still free allocation based on old allocation benchmark

Difference would be covered by carbon contract for difference https://t.co/djF7UWOOpm

Conclusions

-Energy efficiency is not sufficient -Ambition is high for 2030 -It is not possible to focus first on other sectors, new investments must be carbon neutral now.

Questions and answers https://t.co/rtg9jMLhlH